Port Galveston Cruise Terminal 10

Galveston Wharves Cruise Terminal is a two story, 160,000 square-foot terminal building designed to maximize cruise terminal operations while creating a welcoming environment for passengers and crew...

Gain deeper insights into the maritime industry with detailed updates on key developments and trends, meticulously curated by our team of specialists.

Examine how all three major operators absorbed Q1 2026 pressures — and what the diverging results reveal about their structural positions heading into the cycle ahead.

The cruise industry has proven adept at navigating external shocks, and Q1 2026 presented all three major operators with a simultaneous set of pressures. The way each absorbed it reveals how differently the three are now structurally positioned. Last month's BAPerspectives examined this latest shock – the Iran conflict – and its broader impact on the cruise industry. The first-quarter earnings of the three publicly traded North American cruise operators — Royal Caribbean Group (RCG), Carnival Corporation (Carnival), and Norwegian Cruise Line Holdings (NCLH) — bring those macro pressures into focus at the operator level.

All three operators cut full-year 2026 guidance, but for very different reasons and starting points. RCG and Carnival continued to deliver record results and meaningful capital returns from a position of strength, with full-year guidance cuts reflecting modest geopolitical and fuel impacts. NCLH delivered a Q1 that exceeded its own guidance but cut full-year guidance materially as Middle East-related disruption to European demand compounded ongoing execution and commercial-strategy challenges. The Q1 2026 narrative — two operators investing from strength while the third works to close the gap — has hardened into a clear three-way separation.

In this edition of BAPerspectives, we examine how operators absorbed the quarter's pressures, why pricing power is diverging, what each operator's strategic choices signal for the cycle ahead, and what the capital allocation divide means for fleet investment, regional deployment, and forward demand.

Gulf sailing cancellations and 2026/27 redeployment decisions were already underway heading into earnings season, covered in last month's BAPerspectives. What the Q1 calls revealed were two additional impacts. The conflict's disruption to global fuel supply tightened air capacity and pushed airfares higher for North American passengers flying to European embarkation ports, softening Mediterranean bookings late in the quarter. The same supply shock drove marine fuel costs to levels that hit all three operators regardless of where their ships were deployed.

RCG specifically cited increased air travel costs, airline capacity reductions, and flight disruptions as the immediate drivers of softened bookings for high-yielding Mediterranean itineraries late in the quarter. North American demand for European cruising entered the year on an exceptionally strong trajectory, which made the moderation more visible. Because Mediterranean itineraries are concentrated in Q2 and Q3, even a few weeks of softness translated into outsized full-year yield impact. RCG noted that Mediterranean bookings have since rebounded for the limited remaining inventory and that overall, April bookings are running ahead of the same period last year.

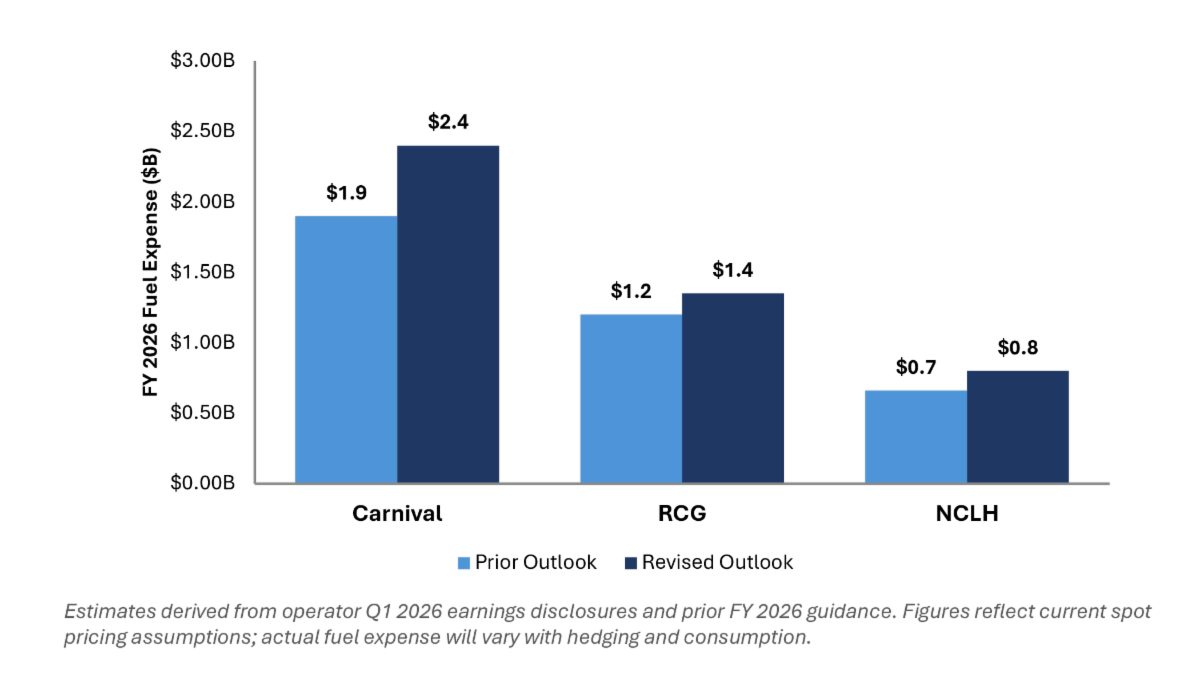

Marine fuel cost was the second shared pressure, and the financial impact varied by hedged position. RCG, with about 60% of consumption hedged, quantified the impact at approximately $0.62 per share for full-year 2026. Carnival faced a roughly $500 million full-year 2026 fuel headwind at current spot prices, partially offset by $150 million of operational improvement. NCLH, the least-hedged of the three, saw fuel hit its full-year outlook by approximately $0.25 per share, with full-year fuel expense now expected at approximately $800 million.

FY 2026 Fuel Expenses – Estimated Increase vs. Prior Outlook

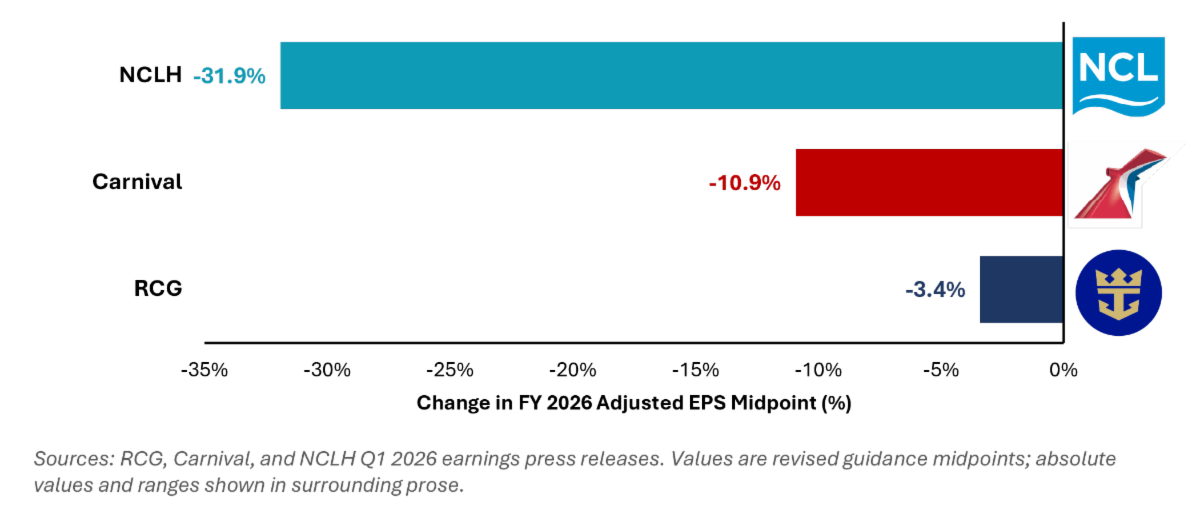

The result was three guidance cuts of materially different scale and structure: a roughly 3% trim at RCG, 11% at Carnival, and 32% at NCLH. For RCG, the cut was modest. Adjusted EPS guidance moved to $17.10–$17.50, still representing 11% year-over-year growth. For Carnival, the headline EPS reduction is essentially a fuel pass-through — the company actually raised its operational outlook by approximately $150 million and reaffirmed $7 billion of full-year adjusted EBITDA. For NCLH, the cut was structural: a midpoint EPS reduction of approximately 32%, combining Middle East-related external pressure with admitted execution gaps in revenue management and commercial strategy.

% Change in Full Year 2026 Adjusted EPS Guidance Cut (Midpoint)

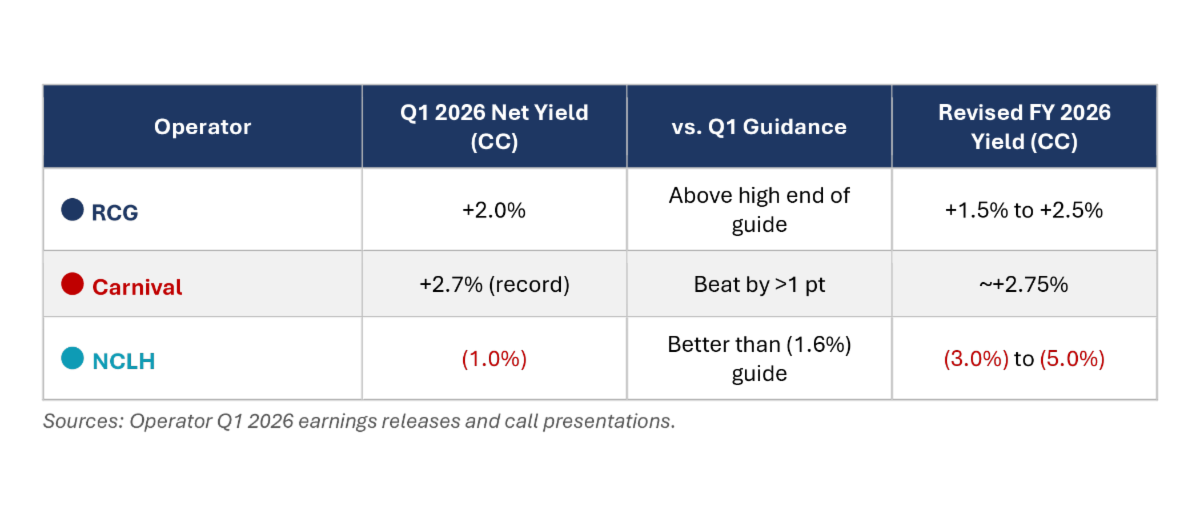

Q1 net yield results were strong-to-record across the sector. Carnival delivered a record Q1 with net yields up 2.7% in constant currency, outperforming guidance by more than a point on what management described as continued strong close-in demand and stronger onboard spending. RCG's net yields grew 2.0% in constant currency, also above the high end of its guidance range, supported by all key itineraries and improved gross margin. NCLH's net yield came in at (1.0%) in constant currency, better than its (1.6%) guide, reflecting the absorption of a 40% year-over-year increase in Caribbean capacity at the Norwegian brand.

The forward outlooks tell the more interesting story. Three distinct positions on the pricing-power spectrum have now emerged.

Net Yield (Constant Currency) – Q1 2026 Actual vs Revised FY 2026 Guidance

Carnival now expects full-year 2026 net yield growth of approximately 2.75%, slightly better than its prior 2.4% guide despite the geopolitical disruption, a notable expression of pricing confidence on top of 2025's record yields. RCG trimmed full-year net yield guidance to 1.5%–2.5% in constant currency, with the revision concentrated in Q2 and Q3 where Med exposure peaks; the full-year outlook still represents healthy growth on top of last year's records. NCLH cut FY net yield guidance to down 3% to 5% in constant currency from approximately flat, the second downward revision in three months and the largest negative outlook from the major operators. NCLH expects Q3 to be its weakest quarter given Europe represents approximately 38% of deployment in the period.

"The pricing-power gap between operators with sustained close-in demand strength and those repricing for execution and demand challenges has not been this wide at any point in the post-recovery cycle."

Carnival used its first quarter to introduce PROPEL (Powering Growth and Returns, Responsibly), a new long-term framework with targets through 2029 designed to reflect continued earnings growth momentum, outsized shareholder distributions, and even higher returns. PROPEL succeeds SEA Change, completed in 2025. Crucially, Carnival announced the new framework in the same quarter it cut full-year EPS guidance, signaling that management views the underlying operational story as strong enough to commit to multi-year ambition through near-term turbulence.

RCG continued executing year two of Perfecta, its 2024–2027 strategic program targeting a 20% earnings CAGR and ROIC in the high teens by 2027. Even with the trimmed full-year guidance, the midpoint of $17.30 represents 11% year-over-year EPS growth, keeping Perfecta on track despite headwinds. CEO Jason Liberty's commentary emphasized the fortified balance sheet, leading margin profile, and continued investment in differentiation as the levers powering through the disruption.

NCLH's quarter was defined by reset, not ambition. CEO John Chidsey, in his first full quarter, announced approximately $125 million of annualized SG&A run-rate savings, a board refreshment with five new independent directors effective March 31, and the previously disclosed cooperation agreement with Elliott Investment Management. The actions were structural: workforce optimization, reduced marketing spend, and a stated focus on aligning resources with the highest-growth, highest-value areas of the business.

"I remain confident and encouraged that we are building a leaner, more effective, and nimble organization that positions NCLH for sustainable long-term value creation."

The framing — leaner, more effective, more nimble — captures NCLH's posture distinctly in that this is repair work, not expansion. Importantly, while a meaningful portion of the SG&A savings is being offset in 2026 by direct costs related to the Middle East conflict (higher crew airfare, elevated logistics costs), all of which are structural in nature. Any savings will carry forward into 2027 and beyond, which is when the benefits to operating margin should become more visible.

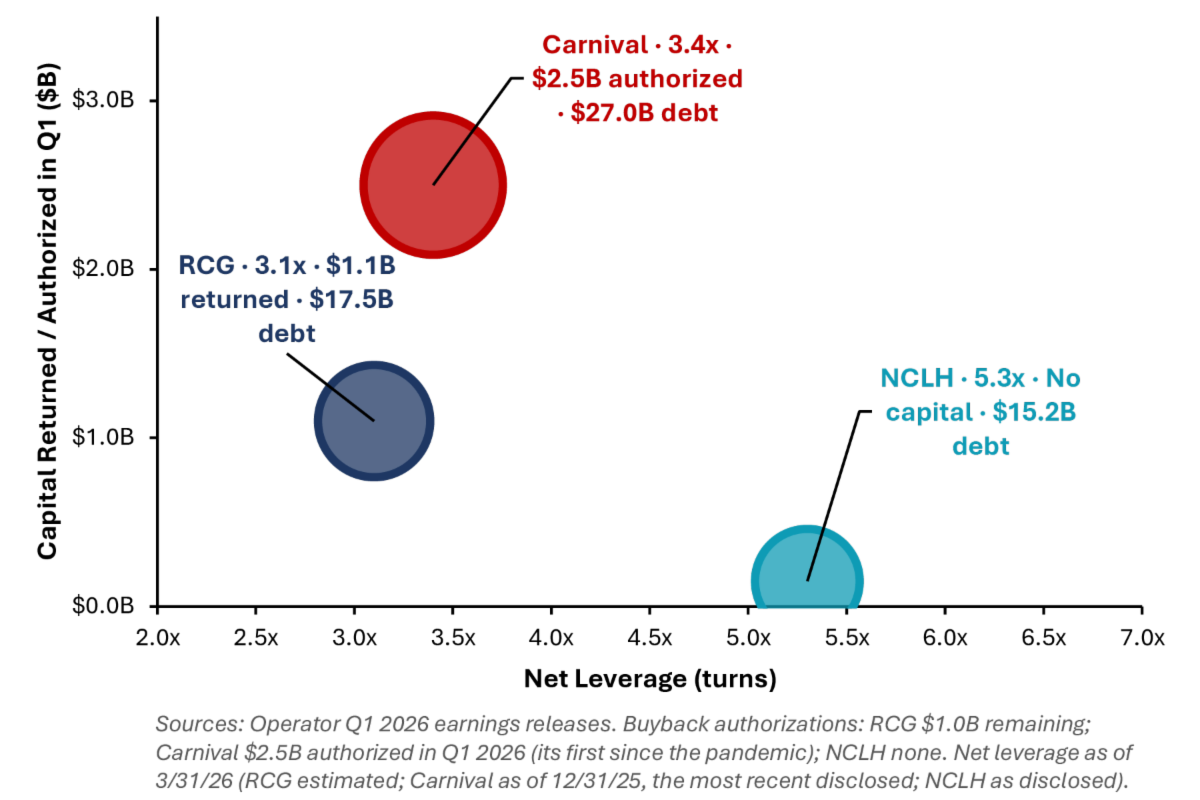

The more telling divide heading into 2026 isn't growth — it's who can return capital to shareholders. RCG returned approximately $1.1 billion to shareholders in the first quarter alone — $836 million through share repurchases and $270 million through dividend payments — with $1.0 billion remaining under the current authorization, against approximately $17.5 billion of total debt and net leverage of roughly 3.1x. The company raised its dividend by 50% in February 2026.

Carnival took a deliberate step into the capital-return cycle, authorizing an initial $2.5 billion share buyback program in Q1 2026, its first since the pandemic, and a milestone made possible by the company's achievement of investment-grade leverage metrics in 2025 (net debt-to-Adjusted EBITDA at 3.4x at year-end and trending lower). The buyback follows the December reinstatement of the dividend disclosed with Q4 2025 results. Carnival carries the largest absolute debt load in the sector at roughly $27 billion, but its leverage trajectory has earned it the capacity to return capital from a position of strength.

NCLH, with net leverage holding at 5.3x as of March 31, 2026 and total debt of $15.2 billion, returned no capital to shareholders. The company's stated capital priority remains balance sheet repair, with deleveraging articulated as a core 2026 focus area.

The Capital Allocation Divide – Q1 2026

"The capital allocation patterns visible in Q1 2026 reflect two to three years of diverging financial trajectories across the three operators, rather than a development specific to this quarter."

Despite the headline guidance cuts, all three operators continued to invest meaningfully in fleet expansion, reinforcing that long-term demand remains intact even as the near-term picture has grown more complex. The orderbook now extends through 2039 with 84 ships on order (240K lower berths on order), representing 32% growth in berths and 19% growth in ships.

RCG announced new orders for Icon 6 and Icon 7 in April 2026, extending the Icon Class through the end of the decade and bumping them into the top position of lower berths on order. The combined fleet pipeline now includes Star of the Seas (delivered), Legend of the Seas (delivering 2026), Hero of the Seas (2027), Icon 5 (2028), Oasis 7 (2028), Celebrity Xcite (2028), and the new Discovery Class (2029 and 2032), in addition to a planned 20 Celebrity River Cruises ships delivering between 2027 and 2031. Q1 2026 capacity was up 8% year over year, with full-year capacity expected to grow approximately 6.7%.

Carnival, by contrast, has held new ship orders to a measured pace, prioritizing same-ship yield growth. Princess's April 2026 order for three ships (delivering 2035–2039) extends Carnival's pipeline into the late 2030s but does not change the near-term growth, anticipated to be less than 1%, the lowest among the three operators.

NCLH took delivery of Norwegian Luna during the first quarter, the latest in its Prima Plus class. NCLH's longer-term order book, extending across its three brands through the mid-2030s, remains among the largest relative pipelines in the industry by ship count, even as near-term financial pressures dominate the immediate narrative.

The Caribbean remains the clearest beneficiary of capacity shifts driven by Middle East caution and softer European demand. RCG's redeployment of Legend of the Seas from Europe to the Caribbean and its leaning into Royal Beach Club Paradise Island illustrate the move among operators with stronger commercial execution; NCLH is shifting in the same direction (Caribbean +10ppt, Europe –5ppt vs. 2025), though the timing has been a near-term yield drag. Bermuda picks up modestly across operators. The West Coast of Mexico, typically a stable alternative, softened alongside the Med during Q1, with RCG citing safety and security concerns tied to a major Mexican Riviera destination served from Los Angeles and San Diego.

Even with the headline guidance cuts, strategic investment in private destinations and exclusive itinerary anchors remain unchanged. As the Q4 2025 BAPerspectives earnings review examined in depth, owned destinations have emerged as a margin-accretive growth engine across all three operators, sitting alongside fleet expansion as a core pillar of the long-term value-creation story. Q1 2026 reinforced that thesis: Royal Beach Club Paradise Island is now operating, Royal Beach Club Santorini opened this past week for visitors, Carnival's Celebration Key continues to ramp up, and NCLH's Great Tides Water Park at Great Stirrup Cay is expected by the end of Q3. Even amid Iran-related disruption and elevated fuel costs, the destination growth strategy remains a structural positive across the sector.

The gap between operationally and financially advantaged operators and those still in repair mode is likely to widen as Q2 unfolds. Carnival and RCG retain the operational and financial flexibility to navigate the headwinds while continuing to invest and return capital to shareholders. NCLH faces a longer road as it works through commercial repositioning, structural cost actions, and balance sheet repair. Key watch items for the coming quarters: Mediterranean booking recovery into the summer/early fall, marine fuel price trajectory and the durability of any Iran de-escalation, NCLH's execution against its restructured framework, and whether the Caribbean continues to be the principal beneficiary of regional capacity shifts driven by ongoing Middle East caution.

Galveston Wharves Cruise Terminal is a two story, 160,000 square-foot terminal building designed to maximize cruise terminal operations while creating a welcoming environment for passengers and crew...

BA's design for the waterfront features a completely transformed Port and Welcome Center, additional mega berths to accommodate the largest cruise ships in the world...

BA was commissioned by RCCL as the architect of record for the new flagship state-of-the-art high-tech Terminal A...

Bermello Ajamil & Partners, Inc. BA, in conjunction with the Renaissance Planning Group, is preparing a Master Plan of the Tampa Port Authority's Waterfront Properties...

Ocean Cay was a 5-year design-build project that BA led as the prime consultant. The ultimate vision for Ocean Cay was to reinvent what a cruise destination island should be for its guests...

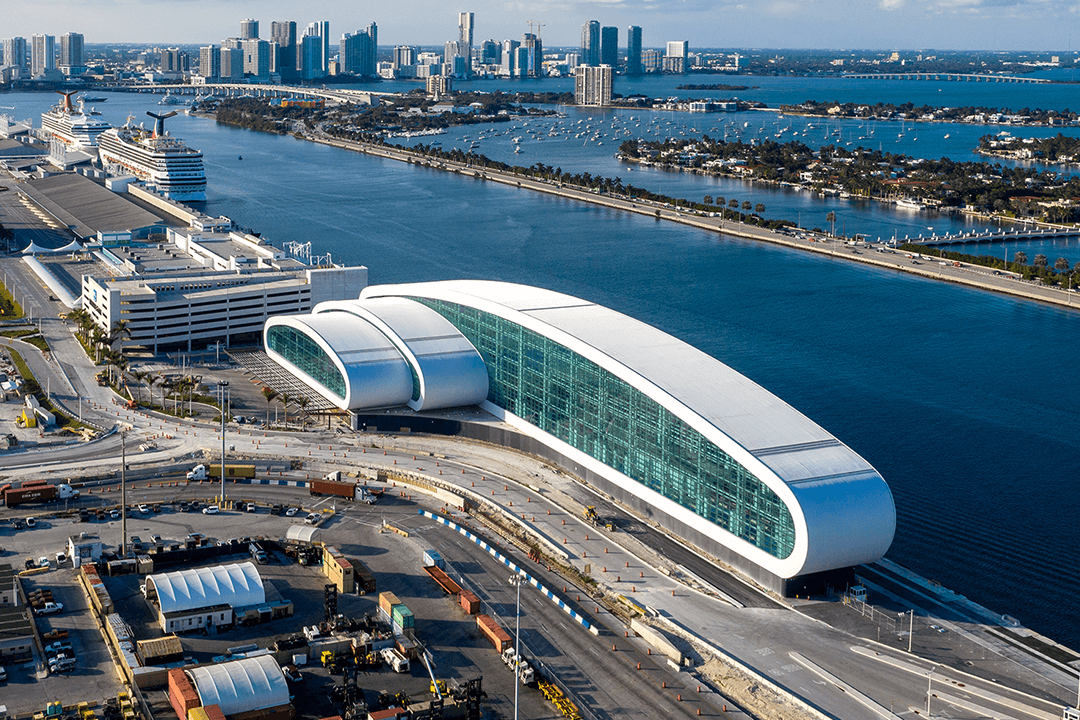

Terminal B accommodates cruise vessels of more than 5,000 passengers, and features new technology to support quicker and more efficient embarkation and disembarkation processes, as well as expedited security screening and luggage check-in...