Port Galveston Cruise Terminal 10

Galveston Wharves Cruise Terminal is a two story, 160,000 square-foot terminal building designed to maximize cruise terminal operations while creating a welcoming environment for passengers and crew...

Gain deeper insights into the maritime industry with detailed updates on key developments and trends, meticulously curated by our team of specialists.

Explore our Q4 and 2025 full-year insights: what does 2026 hold for the cruise industry?

Fiscal year 2025 will be remembered as the strongest in the modern history of the North American cruise industry. Carnival Corporation and Royal Caribbean Group both delivered records on revenues, earnings, and returns on invested capital. Combined, the two largest operators generated approximately $44.5 billion in revenue and $14.2 billion in Adjusted EBITDA. Norwegian Cruise Line Holdings posted solid annual growth — Adjusted EBITDA rose 11% to $2.73 billion and Adjusted EPS climbed 19% — now the company enters 2026 under new leadership, with execution gaps that have opened a widening performance divide among the three largest public cruise operators.

In this edition of BAPerspectives, we examine the themes that defined Q4 and full-year 2025: the industry's record financial performance; the critical test of Caribbean capacity absorption; the balance sheet and market valuation divergence now shaping capital allocation; contrasting fleet investment strategies; and the role of owned destinations as a defining — and cautionary — competitive lever.

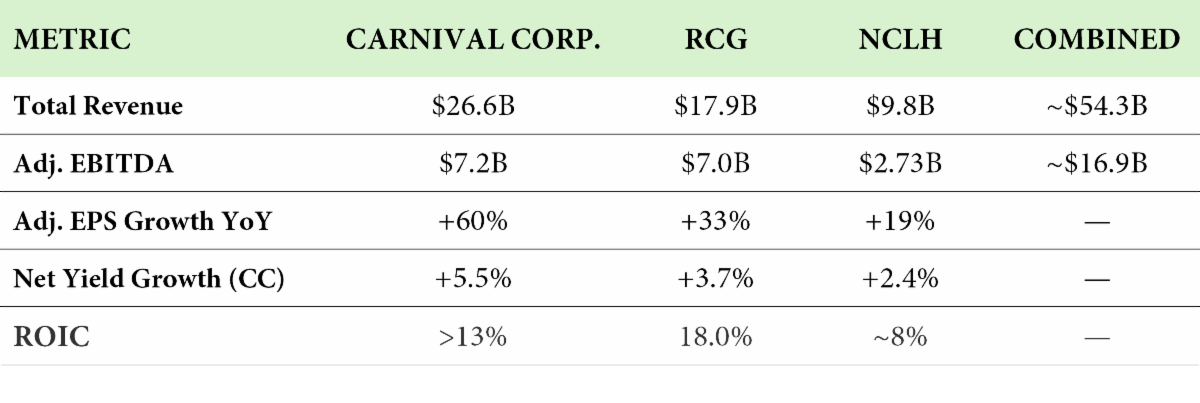

Carnival Corporation delivered full-year revenue of $26.6 billion, Adjusted Net Income of $3.1 billion (up more than 60%), and Adjusted EBITDA of $7.2 billion — each a company record. Adjusted ROIC exceeded 13%, a 19-year high. Royal Caribbean Group posted $17.9 billion in revenue (up 64% versus 2019), $7.0 billion in Adjusted EBITDA (up 94% versus 2019), and Adjusted EPS of $15.64 (+33% YoY), with ROIC reaching 18%. NCLH grew revenue 3.7% to $9.8 billion and increased Adjusted EBITDA 11% to $2.73 billion, exceeding guidance. Q4 specifically saw NCLH deliver net yield growth of 3.8%, Adjusted EBITDA of $564 million (+20%), and Adjusted EPS of $0.28 (+46%). These are not weak results — but set against its peers, the gap is growing.

FY 2025 Financial Highlights

Industry-wide Caribbean capacity grew approximately 27% over two years, raising legitimate questions about pricing power. Carnival, deploying roughly 35% of its total capacity to the region, reported positive yields even as it absorbed a 14% increase in non-Carnival Caribbean capacity. RCG deployed 57% of capacity to the Caribbean and grew regional yields 35% versus 2019. Both operators entered 2026 approximately two-thirds booked at record pricing, with wave season volumes at all-time highs.

NCLH's experience offered a starkly different lesson. The company increased Caribbean capacity approximately 40% in Q1 2026, redeploying vessels to anchor the Norwegian brand around Great Stirrup Cay. But as CEO John Chidsey and CFO Mark Kempa acknowledged, this shift was executed without the cross-functional coordination it required. Revenue management, sales, marketing, and destination readiness were not aligned. Q1 2026 net yields are expected to decline 1.6%, and full-year yield guidance is approximately flat. The contrast reinforces that the Caribbean can absorb significant new capacity — but only when deployment is coupled with disciplined commercial execution.

"Our strategy is sound. Our execution and cross-functional alignment have fallen short. Our priority is to act urgently to address these gaps."

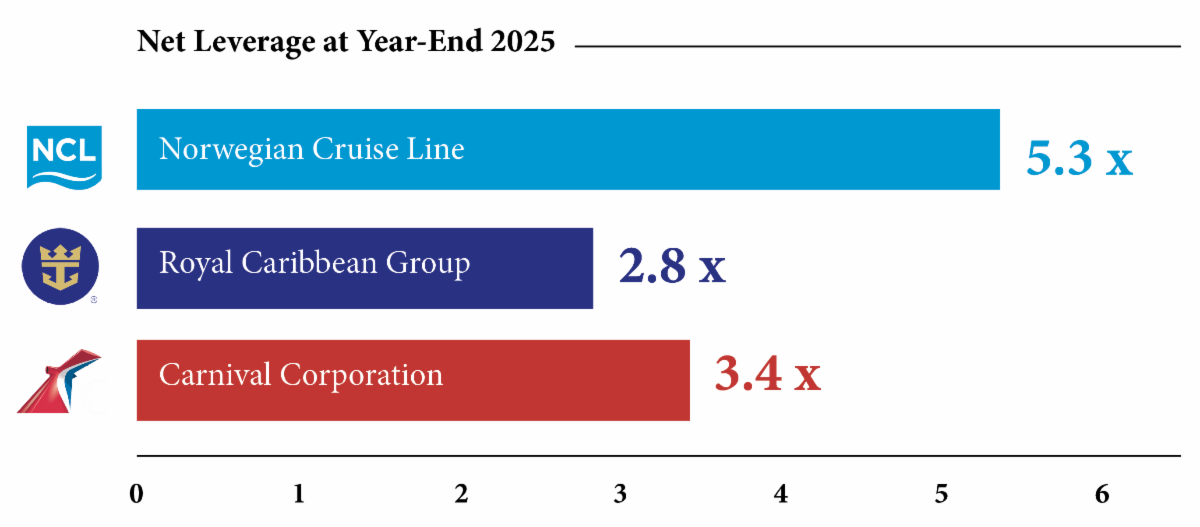

Carnival ended 2025 at 3.4x net leverage, crossing the investment-grade threshold. Fitch has awarded investment-grade status; S&P has the company one notch below with a positive outlook. Debt has been reduced by more than $10 billion from peak, with $19 billion in refinancing activity and over $700 million in projected 2026 interest expense savings versus 2023. The company reinstated a quarterly dividend at $0.15 per share. RCG's transformation is further advanced: investment-grade ratings from all three agencies, leverage below 3x, $6.5 billion in operating cash flow, $2 billion returned to shareholders, and a quarterly dividend raised to $1.50.

NCLH sits on the other side of this divide. Net leverage ended 2025 at 5.3x — nearly double Carnival's ratio — with total debt of $14.6 billion. Leverage is expected to hold flat at approximately 5.2x through 2026 as new ship deliveries temporarily offset EBITDA gains. No dividend. No shareholder return program. Deleveraging remains the top financial priority.

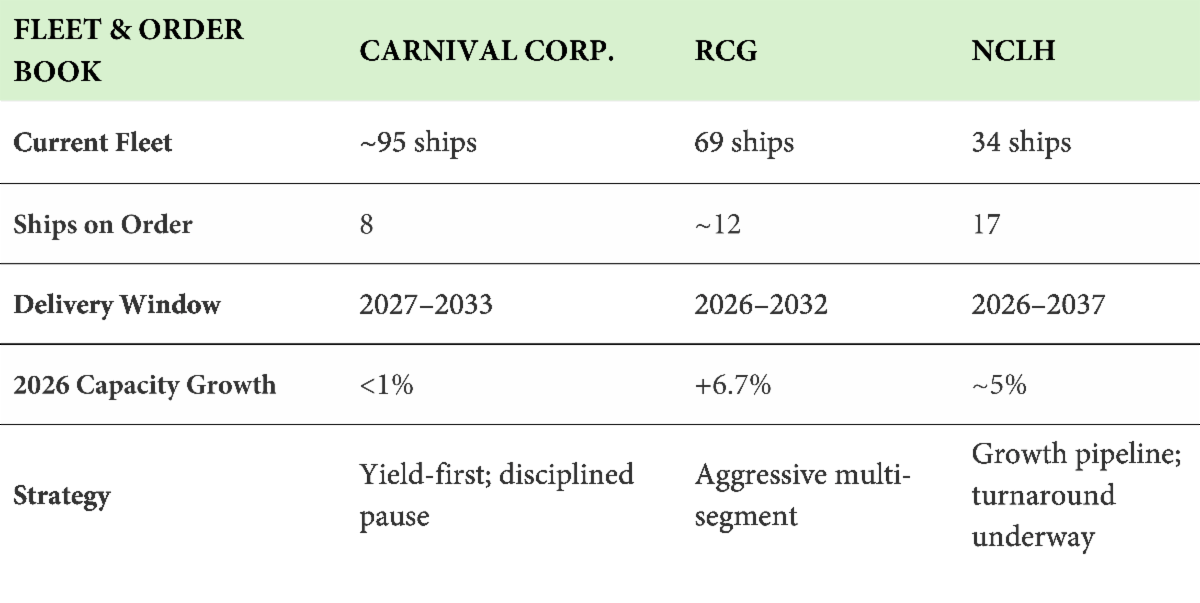

Fleet and Order Book Comparison

The market's pricing of this divergence is unmistakable. As of the writing of this article, RCG trades at approximately $295–$311 per share with a market capitalization of roughly $84 billion. Carnival trades around $29–$31 with a market cap of approximately $44 billion. NCLH trades in the $22–$23 range — near its 52-week lows — at roughly $11 billion. RCG's market cap is nearly eight times NCLH's. NCLH shares fell approximately 8% following the Q4 release, and activist investor Elliott Management, holding a stake exceeding 10%, has been pressing for operational improvements and leadership changes.

RCG is in full expansion mode: approximately 12 ships on order including the newly announced Discovery Class (two firm plus four options, deliveries from 2029), a fifth Icon Class ship for 2028, and Celebrity River Cruises scaling to 20 vessels by 2031. Capacity grows 6.7% in 2026. Carnival is taking the opposite approach by design — no deliveries for 20 months, less than 1% capacity growth, and an order book of just eight ships through 2033. The priority is same-ship yield improvement. NCLH expanded its pipeline to 17 ships through 2037, including three new orders announced this quarter (one per brand). The luxury brands are performing well — Oceania Sonata's opening sales day surpassed the Allura launch by 45%, and Regent recorded its strongest booking month ever in January. But 17 committed ships while carrying 5.3x leverage raises questions about sequencing.

RCG is building the industry's most ambitious destination portfolio: Royal Beach Club Paradise Island opened in December 2025 as Nassau's top-rated experience, with eight destinations planned by 2028 and 20 by 2031. Carnival's Celebration Key surpassed one million guests, with a new pier at Half Moon Cay due mid-2026 and developments in Roatan and Ensenada underway. NCLH's Great Stirrup Cay offers both promise and a cautionary tale — phase one enhancements drew strong guest satisfaction, and the Great Tides Waterpark opens this summer, but the premature deployment of 40% more Caribbean capacity before the island and commercial strategy were ready created the pricing pressure now weighing on 2026 guidance.

"We increased capacity into the region ahead of the full build-out at Great Stirrup Cay. The individual components were moving forward, but they were not integrated under a single cohesive operating plan."

Carnival and RCG are both guiding for double-digit earnings growth in 2026 off record bases, with net yield growth of 2.5% and 1.5–3.5% respectively. Both remain on track for their multi-year financial programs. NCLH is guiding flat yields and 13% EPS growth, driven primarily by cost discipline rather than pricing power. New CEO John Chidsey — two weeks into the role at the time of the call — is conducting an organizational review, with revenue-side improvements likely phasing in during 2027 given the industry's long booking curves.

The industry's structural momentum is unmistakable: more ships, more guests, more destinations, and more revenue per guest than ever before. But this quarter's results make clear that momentum alone is not enough. The gap between the industry's best operators and the rest is widening, and the quality of strategic execution — not just the direction of demand — will determine who captures the next phase of growth.

Galveston Wharves Cruise Terminal is a two story, 160,000 square-foot terminal building designed to maximize cruise terminal operations while creating a welcoming environment for passengers and crew...

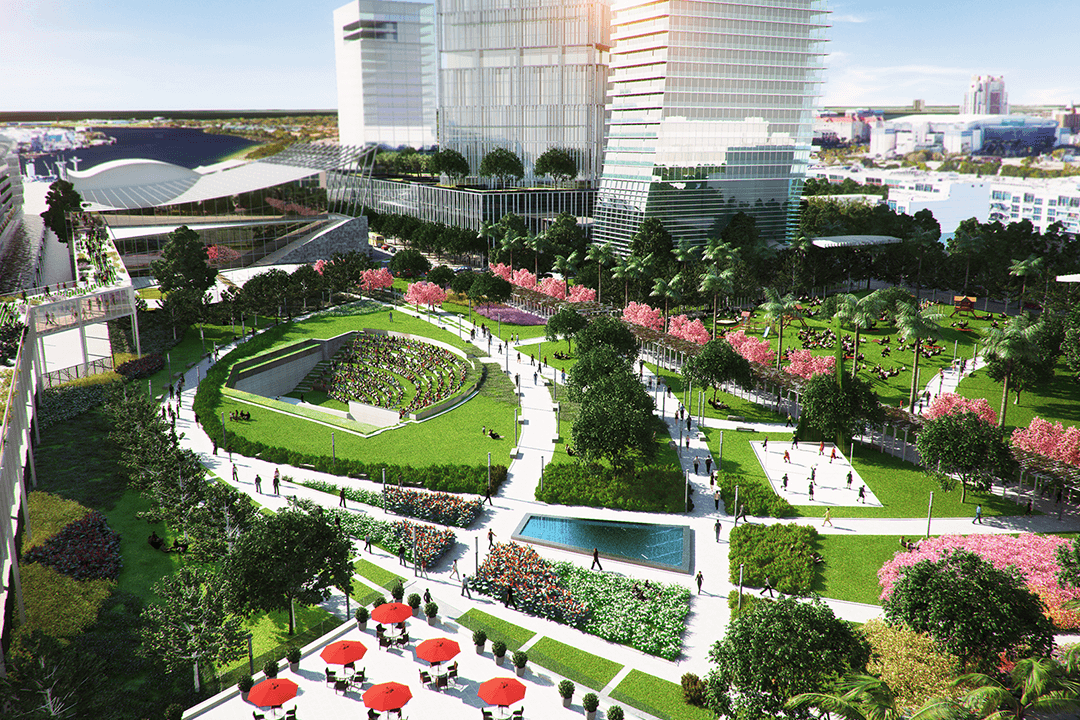

BA's design for the waterfront features a completely transformed Port and Welcome Center, additional mega berths to accommodate the largest cruise ships in the world...

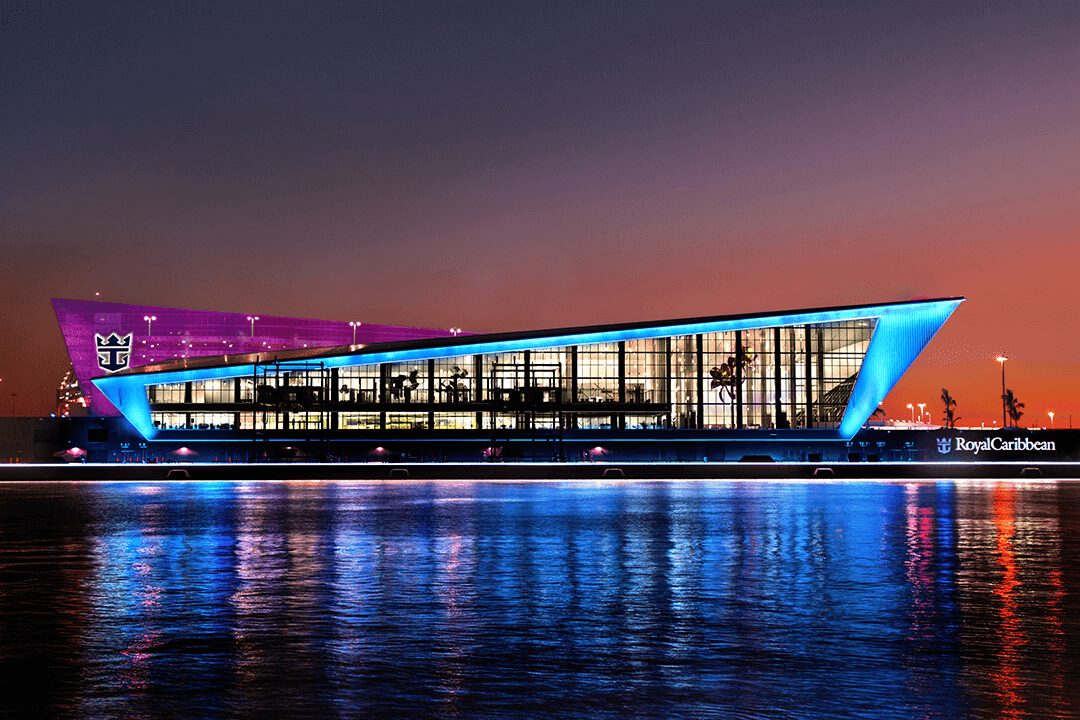

BA was commissioned by RCCL as the architect of record for the new flagship state-of-the-art high-tech Terminal A...

Bermello Ajamil & Partners, Inc. BA, in conjunction with the Renaissance Planning Group, is preparing a Master Plan of the Tampa Port Authority's Waterfront Properties...

Ocean Cay was a 5-year design-build project that BA led as the prime consultant. The ultimate vision for Ocean Cay was to reinvent what a cruise destination island should be for its guests...

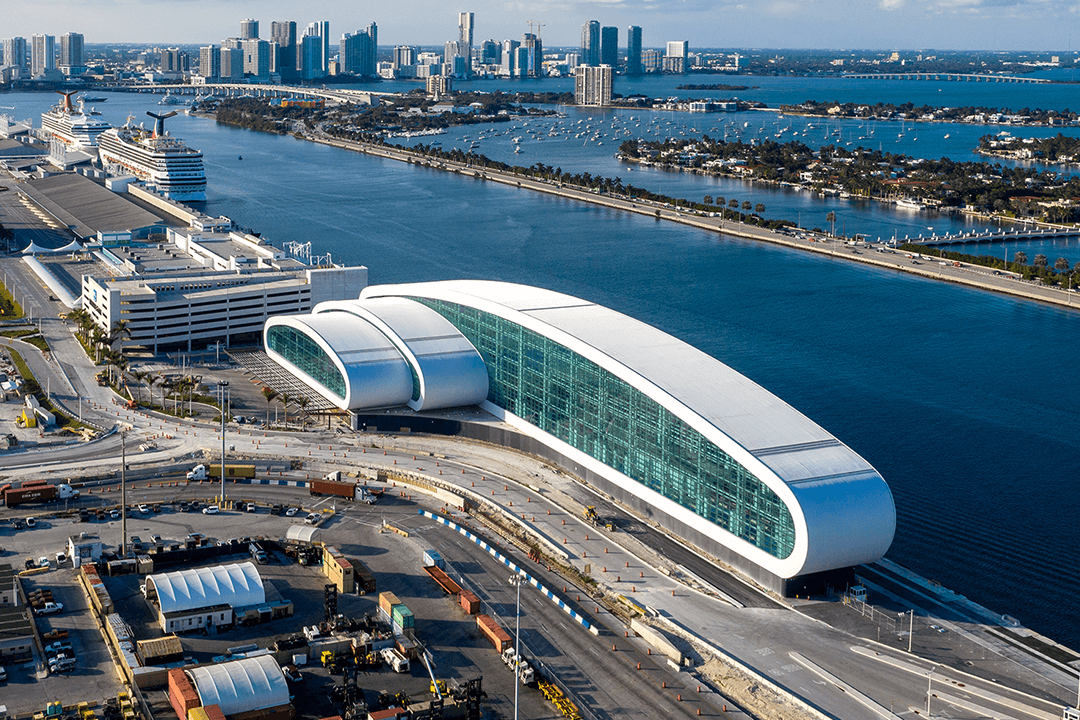

Terminal B accommodates cruise vessels of more than 5,000 passengers, and features new technology to support quicker and more efficient embarkation and disembarkation processes, as well as expedited security screening and luggage check-in...