Port Galveston Cruise Terminal 10

Galveston Wharves Cruise Terminal is a two story, 160,000 square-foot terminal building designed to maximize cruise terminal operations while creating a welcoming environment for passengers and crew...

Gain deeper insights into the maritime industry with detailed updates on key developments and trends, meticulously curated by our team of specialists.

Discover the latest updates on the Iran conflict's impact on cruising—from the Strait of Hormuz to deployment plans and marine fuel costs.

On February 28, coordinated U.S.-Israeli strikes on Iran set off a chain of events that would close the Strait of Hormuz, the only maritime exit from the Arabian Gulf, and trap six cruise ships inside it. At the height of the closure, commercial traffic fell from a normal average of around 138 vessel transits per day to just four to six. Five weeks later, a two-week ceasefire was announced, though subsequent talks failed to produce an agreement and the situation remains volatile. The operational and deployment consequences of the conflict are already underway. Four major brands have cancelled Gulf-bound sailings for the upcoming winter, and marine fuel prices remain well above pre-conflict levels, adding significant costs across the global cruise industry.

In this edition of BAPerspectives, we look at the current state of operations in the region, the near- and medium-term deployment implications, and the broader fuel cost impact that is weighing on the cruise industry today.

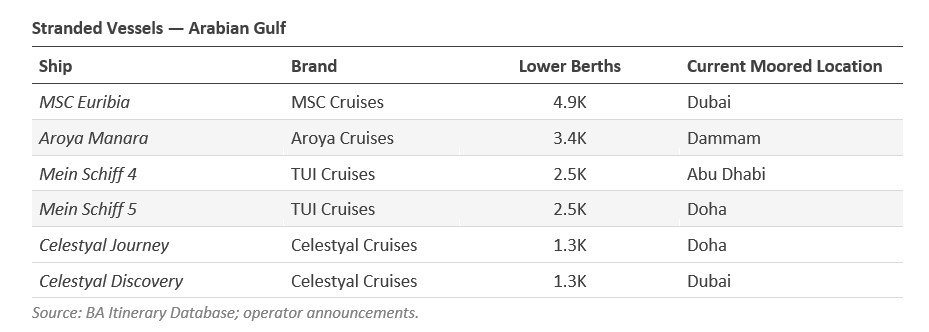

The six stranded cruise ships span four brands and represent more than 15,800 lower berths of capacity sitting idle inside a closed waterway. All passengers have been evacuated, with several ships now operating on skeleton crews. TUI, for example, has reduced staffing aboard Mein Schiff 4 to just 59 of the usual 900 team members.

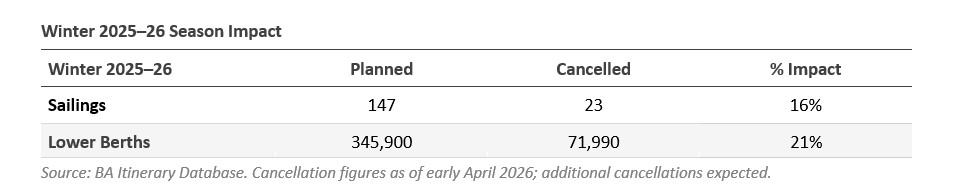

According to BA's itinerary database, 41 sailings have been cancelled in March and April as a result of the closure, representing a combined loss of approximately 100,000 lower berths that were scheduled to sail, with all four impacted operators currently planning to resume sailings in May.

Roughly half of these cancellations are Gulf sailings directly, representing approximately a fifth of the region's total planned winter capacity.

The cancellations are not isolated to the Gulf. Each of the six stranded vessels was scheduled to reposition for summer programs elsewhere: MSC Euribia to Norwegian Fjord sailings from Kiel, the two TUI ships via Cape Town to the Mediterranean, Celestyal's two ships to Greek island programs out of Athens, and Aroya Manara to the Red Sea from Jeddah. With ships unable to reposition, the effects have rippled into subsequent sailings across the Eastern Mediterranean, the Adriatic, and Northern Europe.

The April 8 ceasefire initially raised hopes — cruise stocks surged and oil prices dropped 16% — but the optimism has softened. The Strait remains operating at roughly 10% of normal traffic, with Iran controlling access and in some cases charging tolls of $1 to 2 million per ship for passage through its designated channel. High-level talks broke down on April 12 without an agreement, and the United States has since announced a naval blockade targeting all ships entering or leaving Iranian ports, while stating it will not impede freedom of navigation for vessels transiting the Strait to and from non-Iranian ports. For the stranded cruise ships, the window for repositioning remains uncertain. Even if conditions improve, vessels operating on skeleton crews will need to be fully restaffed and recommissioned before carrying passengers — a process that adds days or weeks depending on the circumstances.

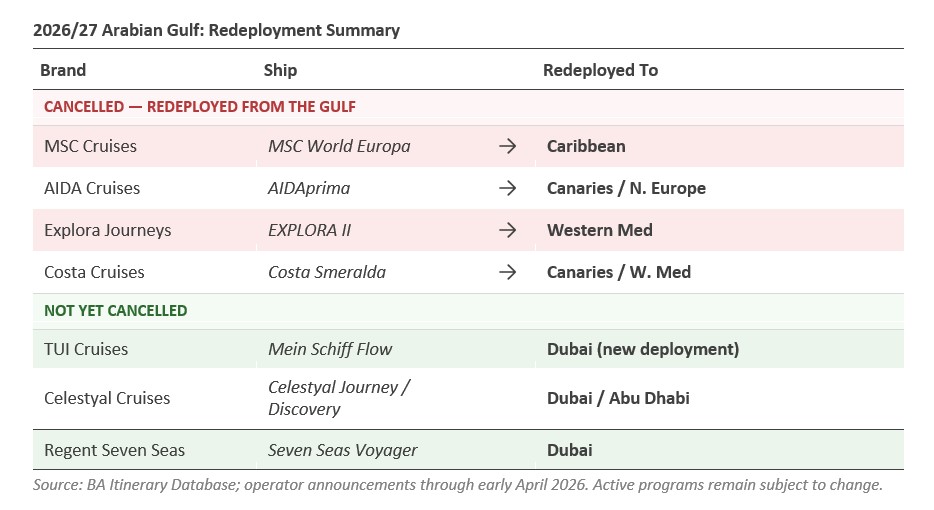

Operators are not just managing the current disruption, they are already making deployment decisions for next winter. Four brands have cancelled Gulf-bound sailings for the 2026/27 season: Costa Cruises, AIDA Cruises, Explora Journeys, and MSC Cruises, redeploying planned regional sailings instead to the Caribbean, Western Mediterranean, Canaries, and Northern Europe. Notably, Europe's two largest cruise groups, Carnival Corporation (via Costa and AIDA) and MSC Group (via MSC and Explora), are among those that have pulled capacity from the region. For these operators, the decision reflects not just the current disruption but a broader caution about committing ships to a region whose near-term stability remains uncertain.

Three brands — TUI Cruises, Celestyal Cruises, and Regent Seven Seas Cruises — have not announced changes to their 2026/27 Gulf programs, though these remain subject to change.

What it takes to bring ships back to the region is tied directly to the length of the conflict, the threat environment for cruise vessels and tourism broadly, and whether operators feel comfortable that the Strait of Hormuz can be counted on as an open and safe waterway. Cruise deployment decisions are made 12 to 18 months in advance: port bookings, shore excursion contracts, crew rotations, marketing, and ticket sales all require long lead times. The ceasefire initially raised hopes, but the latest developments have introduced renewed uncertainty. The industry will need a sustained period of stability before recommitting ships to the region.

On a more positive note, a durable resolution to the conflict could meaningfully benefit the Arabian Gulf's long-term positioning as a cruise market. The region has struggled with volatile cruise traffic tied to recurring geopolitical uncertainty in and around Iran. A sustained period of stability could give operators the confidence to position ships in the Gulf without the risk that has lingered over the region for years. As a secondary benefit, a post-conflict opening of Iran itself — where Iran's Ports and Maritime Organization had been developing cruise tourism infrastructure before the conflict — could expand the regional itinerary map over time, though that scenario remains contingent on outcomes that are far from certain.

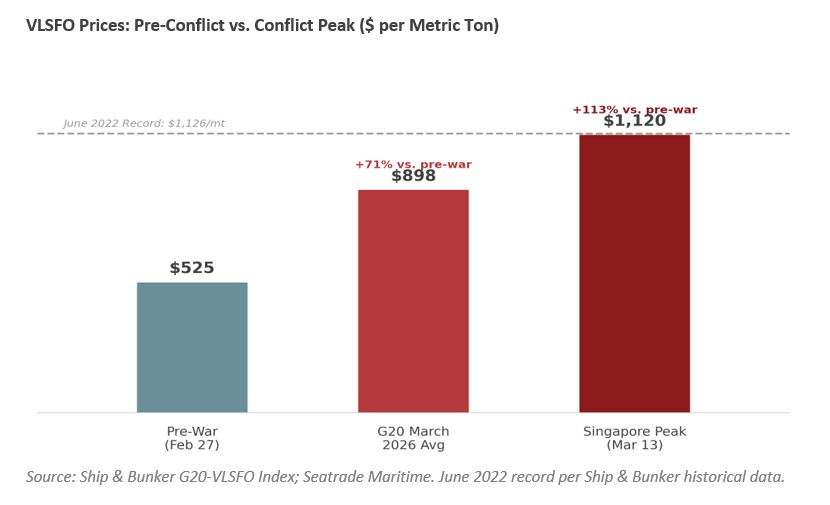

The deployment disruptions are notable, but the conflict's broadest impact on the cruise industry may be economic. The disruption to oil flows through the Strait of Hormuz has driven marine fuel prices to their highest levels since the 2022 Russia-Ukraine crisis. According to Ship & Bunker, VLSFO averaged approximately $898 per metric ton across 20 major bunkering ports in March 2026, up 65% from February. In Singapore, VLSFO briefly touched $1,120 per metric ton on March 13 — a level not seen since June 2022.

Fuel is typically the second- or third-largest operating cost for a cruise line. At current levels, margins are being compressed across the industry regardless of where a given operator's ships are deployed. The financial exposure varies depending on how aggressively operators hedge their fuel purchases — some major lines lock in a significant portion of consumption through forward contracts, while others carry full exposure to spot prices — but no operator is entirely insulated at these levels.

William Blair estimated that rising fuel costs alone could reduce one major operator's full-year earnings by approximately $0.20 per share. Some smaller operators have already introduced fuel surcharges, though the larger lines have so far absorbed the increase rather than pass it directly to consumers.

The broader question is whether this is a short-term spike or a structural shift. The ceasefire initially drove oil prices down sharply, but the collapse of talks sent them back above $100 per barrel, reinforcing the view that fuel relief is tied directly to a diplomatic resolution, not just a pause in fighting. If the conflict resolves and Strait traffic normalizes, fuel markets would likely correct over a period of weeks to months. If it does not, the industry faces a prolonged period of elevated operating costs that could ultimately flow through to ticket pricing, itinerary adjustments to reduce fuel consumption, slower sailing speeds, and a renewed focus on fuel efficiency across the fleet.

The coming weeks will be telling. The ceasefire was an encouraging signal, but the situation continues to evolve. For the cruise industry, the stranded ships remain in the Gulf with no clear timeline for transit. Operators who cancelled 2026/27 Gulf programs appear to be in the clear, and those who have not yet cancelled may soon begin to consider similar action.

Past disruptions offer a useful frame for what may follow. When terrorism struck Tunisia in 2015, cruise traffic to La Goulette halted entirely and did not resume for more than eighteen months. Mexico's cartel violence peak in 2010–2011 drove cruise calls at Mazatlán to zero for three consecutive years. In both cases, recovery followed a similar pattern:

The lesson for the Gulf is that recovery is possible, but it requires sustained stability — not just a ceasefire.

The Gulf's underlying appeal as a cruise market has not changed, but confidence returns slowly once a region has been associated with conflict. With deployment decisions made 12 to 18 months in advance, the window for the 2026/27 season is narrowing fast. How quickly a broader recovery takes shape will depend on the durability of any eventual peace and whether the Strait of Hormuz can once again be treated as an open waterway.

Galveston Wharves Cruise Terminal is a two story, 160,000 square-foot terminal building designed to maximize cruise terminal operations while creating a welcoming environment for passengers and crew...

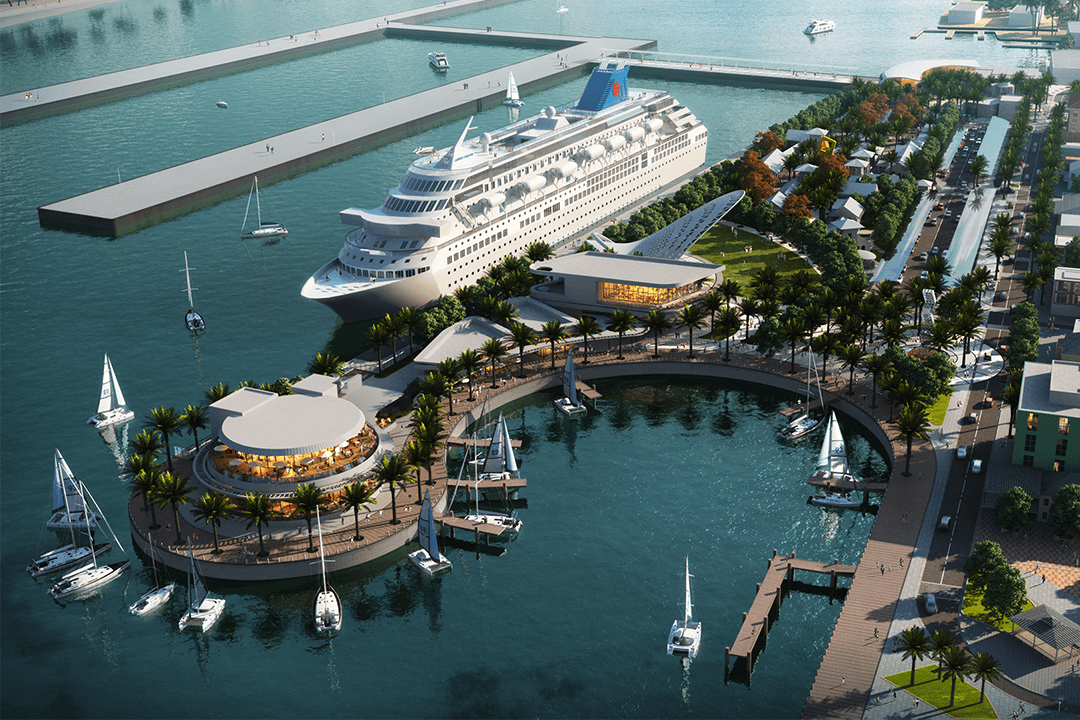

BA's design for the waterfront features a completely transformed Port and Welcome Center, additional mega berths to accommodate the largest cruise ships in the world...

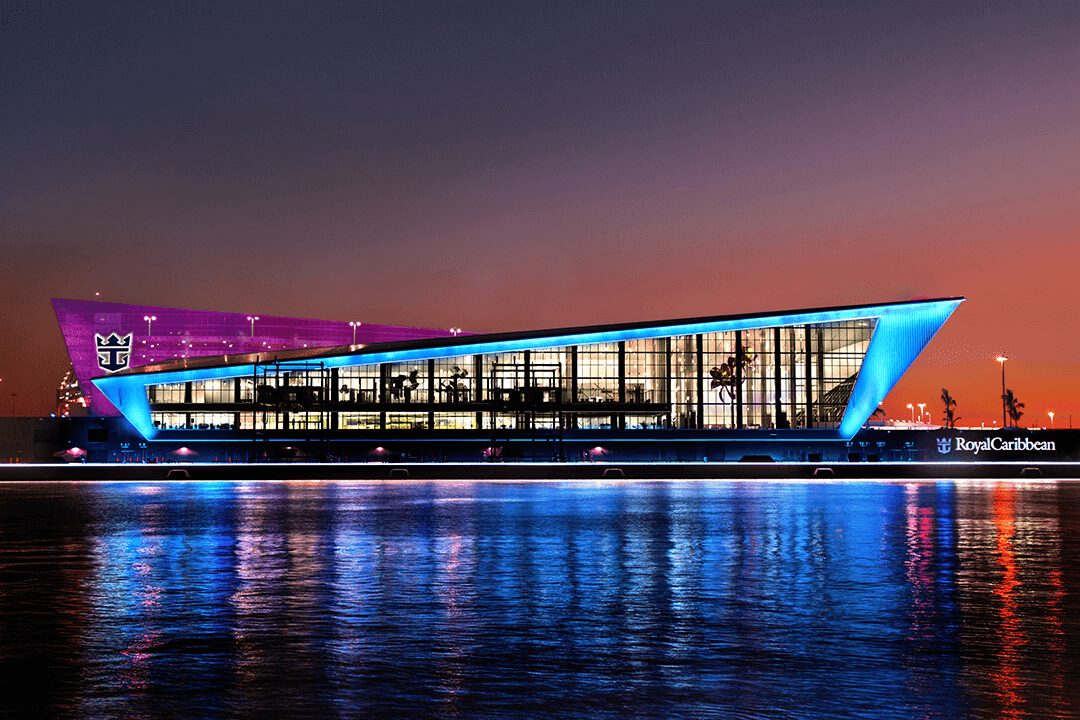

BA was commissioned by RCCL as the architect of record for the new flagship state-of-the-art high-tech Terminal A...

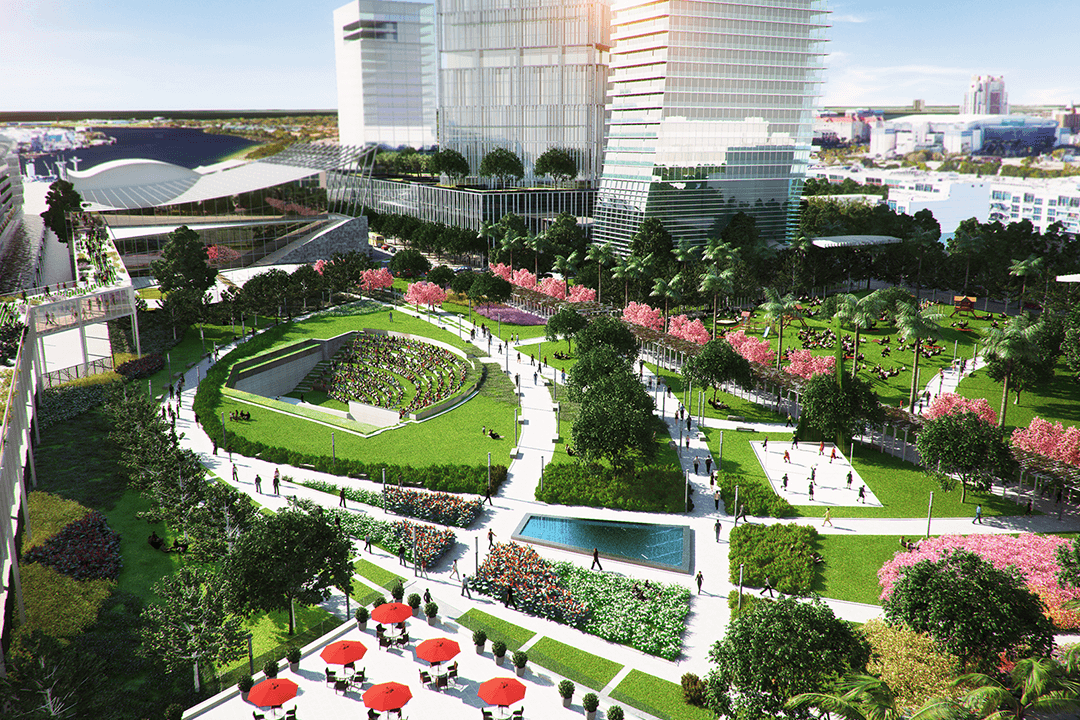

Bermello Ajamil & Partners, Inc. BA, in conjunction with the Renaissance Planning Group, is preparing a Master Plan of the Tampa Port Authority's Waterfront Properties...

Ocean Cay was a 5-year design-build project that BA led as the prime consultant. The ultimate vision for Ocean Cay was to reinvent what a cruise destination island should be for its guests...

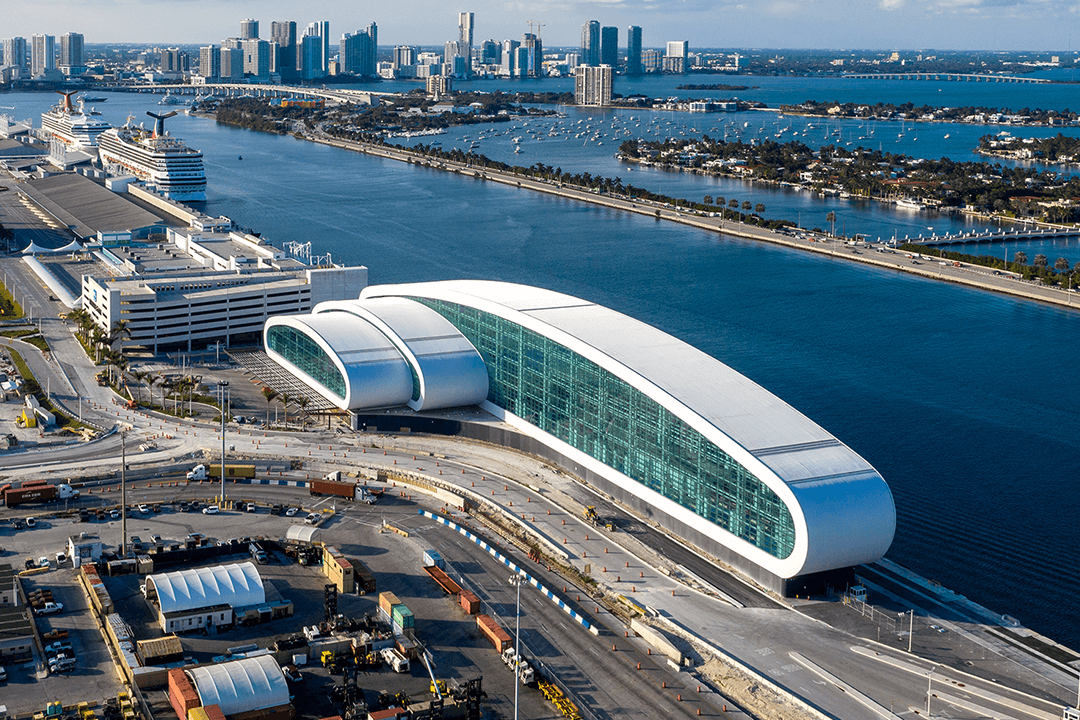

Terminal B accommodates cruise vessels of more than 5,000 passengers, and features new technology to support quicker and more efficient embarkation and disembarkation processes, as well as expedited security screening and luggage check-in...